In the March quarter 2026, the typical Australian small business waited an average of 24.1 days to be paid after issuing an invoice, and invoices were settled an average of 6.9 days late — past their agreed due date (Xero Small Business Insights, March quarter 2026). That short sentence answers the question every owner Googles, but it hides a much bigger story: late payments cost the average Australian SME roughly AU$2,408 a month, or nearly AU$29,000 a year (Airwallex/Censuswide, July 2025); nearly 80% of small and medium businesses reported a cash-flow impact in the past year (CommBank–UNSW, Jan 2025); and from 1 October 2026 the Reserve Bank of Australia is removing card surcharging and cutting interchange fees, a reform that reshapes the economics of getting paid (RBA, March 2026).

This report aggregates the latest verified figures from Xero Small Business Insights, the Payment Times Reporting Regulator, the Reserve Bank of Australia (RBA), the Australian Small Business and Family Enterprise Ombudsman (ASBFEO), the Australian Bureau of Statistics (ABS), CommBank–UNSW, CreditorWatch, ASIC, GoCardless, Airwallex and MYOB into a single, attributed, extractable resource. Every figure is dated and sourced inline.

The headline number: Australian small businesses waited an average of 24.1 days to be paid in the March quarter 2026 and were paid 6.9 days late on average (Xero Small Business Insights). The previous quarter (December 2025) saw 23.9 days to payment — the fastest since Xero began tracking in 2017.

Key statistics at a glance

| Metric | Latest figure | Source | As of |

|---|---|---|---|

| Average time to be paid after invoicing | 24.1 days | Xero Small Business Insights | Mar qtr 2026 |

| Average days paid late (past due) | 6.9 days | Xero Small Business Insights | Mar qtr 2026 |

| Fastest time to be paid on record | 23.9 days | Xero Small Business Insights | Dec qtr 2025 |

| Large-business invoices paid within 30 days | 68.2% | Payment Times Reporting Regulator | Cycle 9 (to Jun 2025) |

| Avg payment time, large biz to small suppliers | 27.4 days | Payment Times Reporting Regulator | Cycle 9 |

| Time to pay 95% of small-biz invoices (95th pctile) | 64 days | Payment Times Reporting Regulator | Cycle 9 |

| SMBs reporting a cash-flow impact in past 12 months | ~80% | CommBank–UNSW (AGSM) | Jan 2025 |

| Average monthly late-payment loss per SME | AU$2,408 (~$29k/yr) | Airwallex/Censuswide | Jul 2025 |

| SMEs losing >$2,500/month to late payments | 17% (up from 11%) | GoCardless | 2025 |

| Time lost chasing payments | ~1.5 hrs/week (~78 hrs/yr) | GoCardless | 2025 |

| Actively trading businesses in Australia | 2,729,648 | ABS | 30 Jun 2025 |

| Small businesses (0–19 employees) | 2,656,469 (97.3%) | ASBFEO / ABS | 30 Jun 2025 |

| Card surcharging removed | 1 October 2026 | RBA | effective date |

| Consumer credit interchange cap | 0.8% → 0.3% | RBA | effective 1 Oct 2026 |

| Consumer savings from surcharge removal | RBA | preliminary |

How long Australian small businesses actually wait to get paid

The single most-asked question among Australian business owners is simple: how long until the money lands? The most current and largest answer comes from Xero Small Business Insights (SBI), a benchmarking series Xero publishes from anonymised, aggregated data from around 520,000 Australian small businesses (Xero Small Business Insights). Because it draws on actual invoice and bank-reconciliation data rather than survey opinions, it is the closest thing Australia has to a live, ground-truth measure of getting-paid behaviour. (The sample size is a point-in-time figure that can shift quarter to quarter.)

In the March quarter 2026 (January–March 2026), the average time to be paid after issuing an invoice was 24.1 days, almost unchanged from the December quarter's 24.0 days (Xero Small Business Insights, March quarter 2026, published ~30 April 2026). Over the same period, invoices were paid an average of 6.9 days late — that is, 6.9 days past whatever due date the business had set — only slightly worse than the 6.7 days late of the December 2025 quarter.

What "days to be paid" and "days late" really mean

These are two different clocks, and confusing them is a common mistake. "Days to be paid" measures the full elapsed time from the moment you issue an invoice to the day cash arrives — it bundles together your payment terms and any lateness. "Days late" isolates only the overshoot beyond the due date. So if you invoice on a 14-day term and the average time to be paid is 24.1 days, roughly 14 of those days are your own terms doing exactly what they were designed to do, and the remaining ~10 days reflect a combination of slow-but-on-time payers and genuine lateness. The 6.9-days-late figure is the part that is truly out of your control — and it is the number that erodes cash flow.

The trend: getting paid faster, but still late

The December quarter 2025 result is historically significant. Australian small businesses waited an average of 23.9 days to be paid — described by Xero as the fastest result since the series began in January 2017 — yet invoices were still paid an average of 6.6 days late that quarter (Xero Small Business Insights, "Small businesses getting paid quicker, but still late"). The headline of that update captures the paradox precisely: payment times have compressed to record speed, but lateness is stubborn. The slight uptick to 24.1 days and 6.9 days late in the March 2026 quarter does not reverse the multi-year improvement; it is well within normal quarter-to-quarter noise.

Why this matters in practice: "6.9 days late" sounds trivial, but on a 14-day invoice it means you are effectively financing your customers for an extra 50% of your stated term — every single invoice, on average. For a business turning over $500,000 a year, roughly $9,000–$10,000 of cash is perpetually "in transit" beyond when it should have arrived.

For longer historical context, an earlier Xero "Crunch" research report (prepared with Accenture, based on 2021 invoice data) found that 48% of invoices issued by Australian small businesses were paid late, with about 1 in 10 (10%) paid more than a month after they were due, at an average of 6.4 days late — and estimated the aggregate cost to Australian small businesses at about $1.1 billion a year (Xero, "Crunch: Cash flow challenges facing small businesses, Part II"). The fact that average lateness has barely moved from 6.4 days (2021) to 6.9 days (2026) — despite record-fast overall payment times — tells you that lateness is a structural feature of Australian trade, not a passing condition.

What big businesses report: the Payment Times Reporting Scheme

Xero measures all small-business invoices; a separate, government-run dataset measures specifically how large businesses pay their small-business suppliers. This is the Payment Times Reporting Scheme (PTRS), administered by the Payment Times Reporting Regulator.

What the scheme is and why it exists

The PTRS, in force since 2021, requires large businesses and certain government enterprises (broadly, those with turnover above $100 million) to publicly report how quickly they pay their small-business suppliers. The policy logic is straightforward: large buyers hold enormous market power over the small firms in their supply chains, and a big customer who stretches payment to 60 or 90 days can starve a small supplier of working capital. By forcing payment behaviour into the open, the scheme creates reputational pressure to pay faster. Following reforms that commenced 7 September 2024 (the Payment Times Reporting Amendment Act 2024 and Rules 2024), the scheme also introduced a clearer accountability mechanism: the Regulator can publicly identify the slowest payers, and the only safe harbour that keeps a reporting entity off the "Slow Small Business Payer" list is having a 95th-percentile payment time of 30 days or less for the reporting period (Payment Times Reporting Regulator, Information Sheet 10). In other words, an entity must clear 95% of its small-business payments within 30 days to be automatically protected from being named, regardless of its industry ranking.

The latest numbers — Reporting Cycle 9

In the most recent Reporting Cycle 9 (1 January – 30 June 2025), the Regulator's January 2026 update reported:

| Metric | Cycle 9 | Prior cycle | Direction |

|---|---|---|---|

| Invoices paid within 30 days | 68.2% | (steady) | flat |

| Invoices paid on time (within terms) | 66.5% | 66.4% | slightly up |

| Average payment time to small suppliers | 27.4 days | 27.1 days | slightly up |

| 95th-percentile payment time | 64 days | 58 days | worse |

| Average common (agreed) payment term | 29 days | 30 days | shorter |

(All figures: Payment Times Reporting Regulator, Regulator's Update January 2026.)

The share of small-business invoices paid within 30 days held steady at 68.2%, and the share paid on time (within whatever terms were agreed) edged up to 66.5% from 66.4% in the prior cycle. The average payment time large businesses took to pay small suppliers was 27.4 days, up slightly from 27.1 days (Payment Times Reporting Regulator, Table 1).

The tail is what hurts: the 95th percentile is getting worse

Averages flatter the picture. The most important figure in the latest cycle is the 95th-percentile payment time, which worsened to 64 days, up from 58 days in the previous cycle (Payment Times Reporting Regulator, media release). The 95th percentile is the time it takes to clear 95% of small-business invoices — in other words, a measure of the slowest payments. While 80% of invoices are paid within 39 days, reaching that final 95% takes 64 days, more than double the 29-day average agreed term (Payment Times Reporting Regulator, Figure 3 / Table 7). It is also worth noting why that 95th-percentile number matters so much under the reformed scheme: it is the exact metric used to decide whether an entity is named a slow payer (the 30-days-or-less safe harbour above), so a tail drifting out to 64 days is precisely what the reforms are designed to expose.

The practical takeaway: the "average" of 27.4 days is misleading for any small business unlucky enough to sit in the slow tail. If you supply a large corporate, your realistic worst-case is a ~64-day wait — over two months — even though the agreed term says 29 days. Price your working capital accordingly.

The long-run improvement is real

Over four years, the proportion of payments made to small-business suppliers within 30 days has risen steadily from 63.2% in June 2021 (Reporting Cycle 1) to 68.2% in June 2025 — a 5.0 percentage-point improvement (Payment Times Reporting Regulator, Figure 5). That is the scheme working as intended: transparency plus the slow-payer accountability mechanism has nudged big buyers to pay faster. In Cycle 9, 3,098 entities reported buying from small-business suppliers, sourcing on average about 28.7% of total procurement from small businesses — highest in construction (43.3%) and lowest in mining (21.1%) (Payment Times Reporting Regulator). That spread matters: a construction subcontractor lives or dies on large-buyer payment behaviour far more than a mining supplier does.

What late payments actually cost

If the time-to-pay figures describe the symptom, the dollar and time costs describe the damage. Here the picture is alarming, and it is getting worse.

The dollar cost per business

Two independent 2025 surveys converge on a similar order of magnitude. An Airwallex/Censuswide survey of 500 Australian SME owners (fielded 23–29 July 2025) found the average loss due to late payments was AU$2,408 every month — nearly AU$29,000 annually, with 84% reporting losses of up to AU$4,999 per month (almost AU$60,000 a year for those owners) (Airwallex, "The Cost of Late Payments Revealed"). The loss scales with size: SMEs earning $50,001–$100,000 a month lost AU$2,569/month, rising to AU$3,055/month for those earning more than $250,000 a month (Airwallex/Censuswide).

Separately, GoCardless's Pursuing Payments 2025 report (YouGov, August 2025, 500 Australian SMBs) found 63% of Australian businesses are losing money to late payments, with some reporting estimated losses over $10,000 per month (GoCardless). Most strikingly, more than 1 in 6 (17%) Australian SMBs estimate losing more than $2,500 per month to late payments in 2025 — up from 11% in 2024, a roughly 55% increase in a single year (GoCardless). And nearly half (48%) say they are waiting longer for payments than they were 12 months ago (GoCardless).

Worked example: Take a landscaping business turning over $30,000 a month. An average loss of ~$2,400/month to late payments equals about 8% of monthly revenue evaporating into financing costs, bad debts, overdraft interest and the owner's unpaid chasing time. Over a year, that ~$29,000 is roughly the cost of a part-time admin hire — or the deposit on a new ute.

The aggregate cost

At the whole-economy level, the most-cited figure remains Xero's estimate that late payments cost Australian small businesses about $1.1 billion per year (based on 2021 invoice data, prepared with Accenture across 200,000+ businesses; Xero "Crunch" Part II, reported by Accountants Daily). It is an older, baseline number — but it is the macro counterpart to the per-business survey figures above, and it is the figure most often quoted in policy debate.

The time cost: chasing payments is a second job

Money is only half the loss; the other half is hours. Among Australian SMBs that chase overdue invoices, the average time lost is about 1.5 hours per week — roughly 78 hours per year, close to two full standard business weeks lost to chasing payments alone (GoCardless Pursuing Payments 2025, via FinTech Australia). The same report finds 63% of Australian SMBs spend time chasing payments, 20% devote 6 to 12 working days a year to it, and 26% spend about an hour every week chasing (GoCardless).

This sits inside a broader admin burden. MYOB/McCrindle research (1,007 Australian SME owners, July 2022) found 83% spend up to 20 hours a month issuing invoices, with 1 in 10 spending 20–49 hours a month on invoicing alone; 62% believed they could save up to 10 hours a week by adopting eInvoicing, and MYOB frames saving 5 hours/week as 260 hours — 10 full working days — a year (MYOB). More broadly, SME owners are often estimated to spend several hours each week on finance and administration (Dext "Built for Bigger Things" 2025, via ScaleSuite — treat as indicative).

Late payments are the single biggest dispute

How much late-payment friction consumes small businesses' attention is captured in one striking statistic: payment disputes are the single largest category of cases brought to the ASBFEO, accounting for 42% of total assistance requests in 2023–24, up from a historical average of about 26% (ASBFEO assistance data, via SmartCompany). When more than four in ten of all the complaints reaching the small-business ombudsman are about getting paid, it is no longer a back-office nuisance — it is the defining operational risk of running a small Australian business.

The cash-flow squeeze behind the numbers

Late payments don't exist in a vacuum; they are the sharpest edge of a broader cash-flow squeeze. The joint CommBank–UNSW (AGSM) survey (YouGov, n=507 Australian SMB owners/decision-makers, fieldwork 31 October – 5 November 2024, published 16 January 2025) found that nearly 80% of Australian SMBs experienced an impact to their cash flow in the last 12 months (UNSW Newsroom).

How owners cope — and why it's worrying

Crucially, the survey reveals how owners absorb the shock. 27% said they dipped into personal savings or didn't pay themselves a salary (or both) in the last year just to keep the business running (CommBank–UNSW). That single figure is the human face of the cash-flow data: when a customer pays 64 days late, it is often the owner's own household that bridges the gap. A further 25% used "increasing sales and/or pricing" as a cash-flow management strategy — meaning a quarter of businesses are effectively passing late-payment costs on to all their customers through higher prices (CommBank–UNSW). Other coping strategies included reviewing or decreasing expenses (34%), maintaining a cash reserve (27%) and finding additional revenue streams (26%).

The top causes of cash-flow stress were declining revenue (35%), low cash reserves (30%) and seasonal fluctuations (27%) (CommBank–UNSW). Late payment compounds every one of these — a business with thin reserves and a seasonal dip is exactly the one a 64-day-late invoice can tip over.

Corroborating evidence

An earlier Xero/Insights Exchange study (fieldwork January 2023) found 60% of surveyed Australian small businesses had experienced cash-flow issues, with 14% describing them as "significant," and 27% said they had to use personal savings to stay afloat (Xero AU media release). The consistency of that 27% personal-savings figure across two independent surveys, two years apart, suggests it is a stable structural feature: roughly one in four Australian small-business owners self-funds the business through their own savings to survive cash-flow gaps.

The downstream risk: tax debt, insolvency and closures

When cash-flow stress is sustained, the end point is closure — and the data here is sobering, though there are early signs of relief.

The business population: context first

There were 2,729,648 actively trading businesses in Australia at 30 June 2025, up 2.5% (66,650 businesses) over the year (ABS Counts of Australian Businesses). Of these, 994,178 were employing and 1,735,470 (about 63.6%) were non-employing — sole traders and owner-operators with no staff. Small businesses (0–19 employees) made up 97.3% of all Australian businesses, totalling 2,656,469 (ASBFEO/ABS): 63.6% non-employing, 25.2% with 1–4 employees, and 8.5% with 5–19 employees. Australians started 437,150 new businesses in 2024–25 (a 16.4% entry rate) while 370,500 exited (a 13.9% exit rate) (ABS). The business count has grown steadily — from 2,402,254 in June 2021 to 2,662,998 in June 2024 to 2,729,648 in June 2025 (ABS).

Why the 97.3% figure matters: when nearly every Australian business is small and almost two-thirds have no employees, the late-payment problem is not a fringe concern — it is the dominant operating reality of the entire business sector. There is no big back-office to absorb a 64-day-late invoice; it lands directly on the owner.

Survival rates favour employers

Business survival differs sharply by employer status. Of businesses that started in 2021–22, after one year 82.4% of employing businesses were still operating versus 72.3% of non-employing; by year three the gap widened to 61.0% versus 43.3% — a 17.7 percentage-point survival advantage for employing businesses (ABS survival data, via ScaleSuite). Cash-flow management is a large part of that gap: employing businesses tend to have more formal financial systems and credit access to weather payment delays.

Insolvencies hit a record, then began to ease

Company failures surged through 2024–25. Companies entering external administration for the first time hit a record 14,722 in FY2024–25, up 33.2% from 11,053 the prior year (ASIC, via commentary). In the 12 months to 31 May 2025, 13,413 companies entered external administration — up 34.2% year-on-year — lifting the insolvency rate to 0.41% of the 3,538,524 registered companies (from 0.32%), though still below the 2011–12 and 2012–13 peaks of 0.56% and 0.53% (ASIC Corporate Insolvency Update Issue 36).

Then the tide turned. 3,556 companies entered external administration in Q1 FY2025–26, down 2.1% year-on-year (ASIC, via Murrays Legal). CreditorWatch's Business Risk Index recorded 1,051 first-time insolvencies in May 2026 — the lowest monthly figure in nearly two years — with insolvencies running about 4% lower across the first 11 months of FY2025–26 and the national insolvency rate at roughly 0.5% of companies (CreditorWatch, May 2026).

Which sectors are worst hit

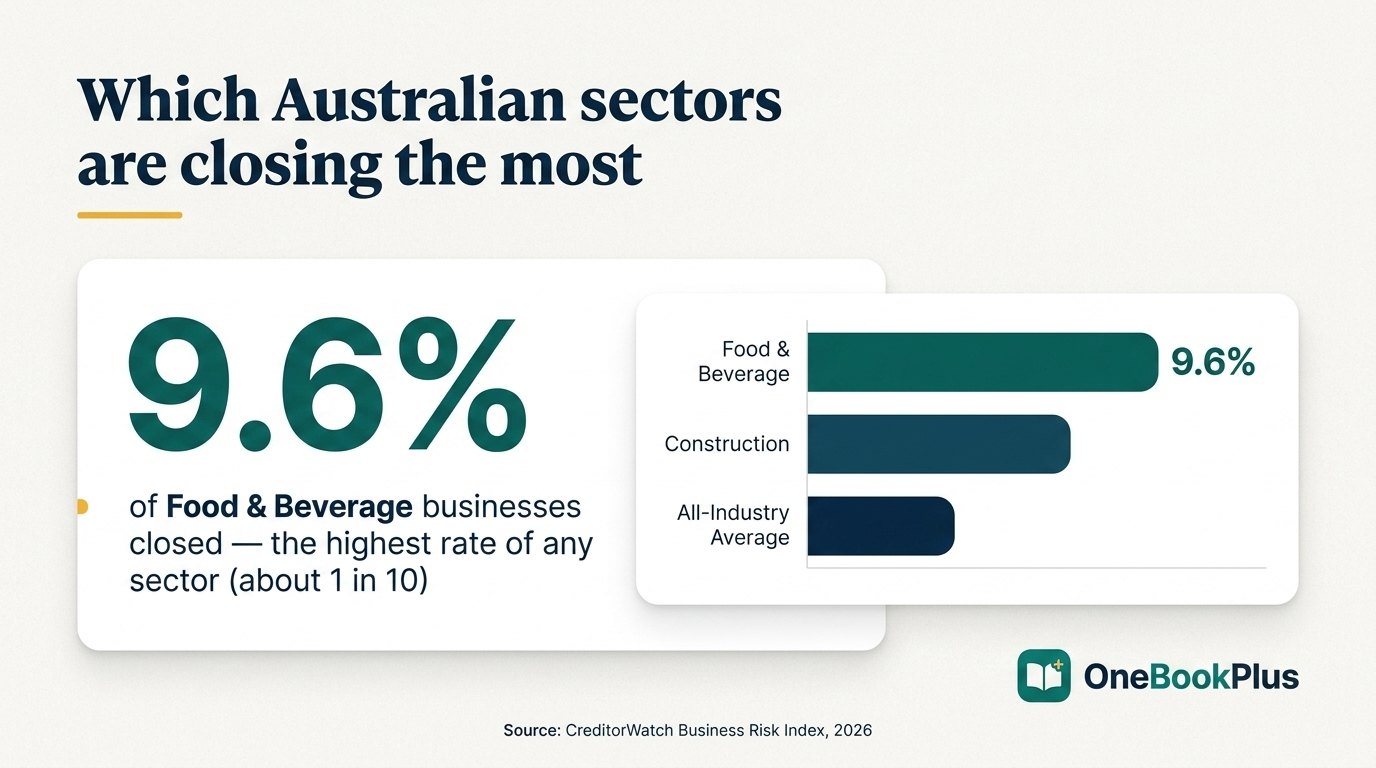

The pain is concentrated. Food & Beverage Services is the worst-affected sector, with a record 9.6% of businesses in the sector closing over the prior 12 months — roughly 1 in 10 hospitality businesses — and it ranks highest across insolvency rates, arrears (late payments) and ATO tax-debt defaults over $100,000 (CreditorWatch, April 2026). Construction and Food & Beverage combined account for around 40% of all insolvencies over the past year (CreditorWatch). The ASIC industry breakdown for FY2023–24 tells a similar story: Construction at 27% (2,975 companies), Accommodation & Food Services at 15% (1,667) and Other Services at 9% (1,039) — together more than half of all administrations (ASIC). In the most recent BRI, Waste Services emerged as a deepening stress point, its insolvency rate now more than three times the national average (CreditorWatch, May 2026). Forecast 12-month closure rates vary sharply by location: up to 7.90% in the highest-risk area (Bringelly–Green Valley, Western Sydney) versus 4.57% in the lowest (Norwood–Payneham–St Peters, Adelaide) (CreditorWatch).

The ATO tax-debt early-warning signal

The clearest leading indicator of failure is unpaid tax. An ATO tax-debt default — defined for credit-reporting as a debt exceeding $100,000 that is more than 90 days overdue, which the ATO discloses to credit bureaus — is a powerful predictor: businesses with an ATO tax default are many times more likely to go insolvent within 12 months than those without (CreditorWatch). And 33.6% of private businesses with such a default (1,715 of 5,097) had become insolvent or voluntarily closed over the prior year (CreditorWatch, December 2024). The number of companies with ATO tax defaults climbed from roughly 30,000 to about 36,000 — nearly a 20% increase — over six months (CreditorWatch, May 2026). For context, total ATO outstanding tax liabilities were reported at around $52 billion, of which a large share was owed by small and medium businesses (via Accountants Daily). The mechanism is intuitive: a business that can't pay the tax office is usually a business already drowning in a late-payment cash-flow gap.

The news hook: the RBA card-surcharge ban and interchange cuts

The most consequential change to the economics of getting paid in a decade takes effect on 1 October 2026. After a review launched in October 2024 and extensive consultation (over 170 written submissions and 100+ stakeholder meetings on the July 2025 Consultation Paper alone), the RBA's Payments System Board concluded it will remove surcharging on debit, prepaid and credit cards across the designated eftpos, Mastercard and Visa networks, and lower interchange fee caps (RBA Media Release MR-26-10, March 2026).

What changes, and when

- Card surcharging removed on eftpos, Mastercard and Visa debit and credit cards — from 1 October 2026 (RBA).

- Lower domestic interchange caps — also from 1 October 2026 (RBA).

- Foreign-card interchange cap (1.0%) and transparency measures — from 1 April 2027 (RBA).

The interchange changes are specific. Consumer credit interchange is cut from 0.8% to 0.3% of transaction value (a 0.5 percentage-point reduction), and the separate 0.5% weighted-average benchmark is abolished (RBA, Conclusions Paper Ch.3). Consumer debit and prepaid caps fall from 10 cents (or 0.2%) to 8 cents (or 0.16%). Commercial credit is retained at 0.8%, and a new single cap of 1.0% applies to all foreign-issued cards (from 1 April 2027) (RBA).

"Interchange" defined: interchange is the wholesale fee your payment processor pays the customer's card-issuing bank on every transaction — it is the largest component of what you, the merchant, ultimately pay to accept a card. Lower interchange caps mean lower merchant fees, flowing through over time.

What it's worth — to businesses and consumers

Australians currently pay an estimated $1.8 billion a year in card surcharges on the designated networks, of which consumers pay about $1.6 billion ($0.2 billion paid by businesses); surcharging has roughly doubled since 2022, and about 16% of merchants currently surcharge (RBA Conclusions Paper). Removing it, preliminary RBA estimates indicate, would see consumers pay around $1.2 billion less in surcharges per year — about $60 per card-using adult (RBA Consultation Paper, July 2025).

For merchants, the lower interchange caps will reduce wholesale card payment costs by around $910 million per year, and the RBA states small businesses benefit most because they tend to pay fees closest to the existing caps (RBA). Small merchants would be better off by around $185 million versus the current framework, with about 90% benefiting in net terms (RBA Consultation Paper). The final Conclusions Paper notes that 85% of small merchants do not surcharge (and 89% of large merchants), so the surcharge removal affects few of them directly, while the interchange cuts flow broadly (RBA, Ch.8). The one-off implementation cost of removing surcharging on all cards is about $25 million (versus ~$45 million for debit-only), and the one-off price-level (inflation) effect, if fully passed into sticker prices, is around 0.1% (RBA).

Why this matters for getting paid

The connection is direct. A major reason some businesses hesitate to offer card or "Pay now" payment options is the cost — and the awkwardness of surcharging customers. Once surcharging is gone and interchange is lower, the friction and expense of accepting cards both fall. That matters because online and card payment is the single most effective lever a small business has to get paid faster: Xero reports businesses that add a "Pay now" button get paid up to twice as fast, customers pay three times faster with Apple Pay or Google Pay, and SMS invoices can be paid up to 3x faster than email invoices without payment services (Xero AU). With the surcharge barrier removed from 1 October 2026, that speed advantage becomes cheaper and easier to deploy.

How Australian businesses get paid — methods, terms and what speeds it up

The payment-method mix is shifting

Cards remain the most-used consumer payment method, but their share is slipping — from 76% of payments by number in 2022 to about 73% in 2025; debit cards alone account for about 49% (roughly one in two payments) and credit cards about 23% (RBA, 2025 Consumer Payments Survey). Cash made up about 15% by number in 2025 (up from 13% in 2022) but only around 8% by value, and 43% of consumers used a mobile device for a contactless payment during the diary week, up from 35% in 2022 (RBA). The clear direction of travel: digital, mobile-wallet and card payments dominate the small-ticket transactions most small businesses live on.

Terms: shorter is better

On payment terms, the guidance is consistent. Xero recommends 7- to 14-day terms, noting invoices with one-week terms are paid in about two weeks — faster than voluntarily waiting 30 days even if paid late (Xero AU). MYOB notes the Business Council of Australia's supplier payment code calls for small-business suppliers to be paid within 30 days, with terms ranging from as short as 7 days to occasionally 90–120 days, though the majority see no reason to offer terms longer than 30 days (MYOB). The logic is simple arithmetic: if average lateness is ~7 days, a 7-day term gets you paid around day 14, while a 30-day term gets you paid around day 37 — the shorter term wins even though both are "late."

Levers that demonstrably speed up payment

- Online "Pay now" options: paid up to 2x faster (Xero).

- Apple Pay / Google Pay: customers pay 3x faster on average (Xero).

- SMS invoices: paid up to 3x faster than email (Xero).

- Fast settlement: card/Stripe/GoCardless funds typically reach the bank account in 1–2 (up to 3) business days (Xero).

- Credit-signalling on invoices: CreditorWatch reports customers who placed its logo on invoices saw a 53% increased chance of payment and a 7-day reduction in time to pay (MYOB/CreditorWatch — vendor-reported).

The throughline of every credible source is the same: the cheapest, fastest way to fix late payment is to remove friction from the act of paying — offer instant online payment, send the invoice where it gets seen, and keep terms tight. Modern all-in-one tools that combine invoicing, "Pay now" links and automated reminders — OneBookPlus among them — exist precisely to compress that 24-day average and shave days off the 6.9-day lateness gap.

Frequently asked questions

How long do Australian small businesses wait to get paid in 2026?

In the March quarter 2026, Australian small businesses waited an average of 24.1 days to be paid after issuing an invoice, and invoices were settled an average of 6.9 days late — past their agreed due date (Xero Small Business Insights). The December 2025 quarter recorded 23.9 days, the fastest result since Xero began tracking in January 2017. These figures are derived from anonymised, aggregated data from around 520,000 Australian small businesses.

What does late payment actually cost an Australian small business?

The average Australian SME loses about AU$2,408 a month to late payments — nearly AU$29,000 a year — according to an Airwallex/Censuswide survey of 500 SMEs in July 2025. More than 1 in 6 (17%) lose over $2,500 a month, up sharply from 11% in 2024 (GoCardless), and 63% of businesses report losing money to late payments. At the whole-economy level, Xero has estimated late payments cost Australian small businesses about $1.1 billion a year (based on 2021 invoice data).

What share of invoices do large businesses pay on time to small suppliers?

In Reporting Cycle 9 (to June 2025), large businesses paid 66.5% of small-business invoices on time (within agreed terms) and 68.2% within 30 days, taking an average of 27.4 days, according to the Payment Times Reporting Regulator. However, the 95th-percentile payment time — the slowest tail — worsened to 64 days, more than double the 29-day average agreed term, meaning the slowest payments are getting slower even as averages improve.

What is the RBA card-surcharge ban and when does it start?

From 1 October 2026, the RBA is removing surcharging on eftpos, Mastercard and Visa debit, prepaid and credit cards, and lowering interchange fee caps — for example, consumer credit interchange falls from 0.8% to 0.3% of transaction value. The reform is expected to reduce merchants' wholesale card costs by about $910 million a year and save consumers around $1.2 billion a year (about $60 per card-using adult). A new 1.0% cap on foreign-issued cards and transparency measures follow on 1 April 2027.

How much time do small business owners spend chasing late payments?

Australian SMBs that chase overdue invoices lose about 1.5 hours a week — roughly 78 hours a year, close to two full standard business weeks — according to GoCardless's Pursuing Payments 2025 report. About 63% of SMBs spend time chasing payments, 20% devote 6 to 12 working days a year to it, and payment disputes are now the single largest category of cases brought to the ASBFEO, at 42% of all assistance requests in 2023–24.

Which industries are most affected by closures and insolvency in 2026?

Food & Beverage Services is the hardest-hit sector, with a record 9.6% of businesses closing over the prior 12 months — about 1 in 10 hospitality businesses — and it ranks highest for insolvencies, arrears and large ATO tax defaults (CreditorWatch). Construction and Food & Beverage together account for around 40% of all insolvencies. Waste Services has emerged as a new stress point, with an insolvency rate now more than three times the national average.

Does offering online or card payment really get you paid faster?

Yes. Xero reports that small businesses adding an online 'Pay now' option get paid up to twice as fast, customers pay three times faster on average with Apple Pay or Google Pay, and SMS invoices can be paid up to 3x faster than email invoices without payment services. Online providers typically settle funds to a bank account within 1–2 business days. Keeping terms short (Xero recommends 7–14 days) and removing payment friction are the most effective levers a small business has to improve cash flow.

How many small businesses are there in Australia?

There were 2,729,648 actively trading businesses in Australia at 30 June 2025, up 2.5% over the year (ABS). Small businesses with 0–19 employees made up 97.3% of all businesses, totalling 2,656,469 (ASBFEO/ABS), and about 63.6% of all businesses are non-employing sole traders. Survival rates favour employers: of businesses started in 2021–22, 61.0% of employing businesses survived to year three versus just 43.3% of non-employing ones.